Dear NMA Supporter,

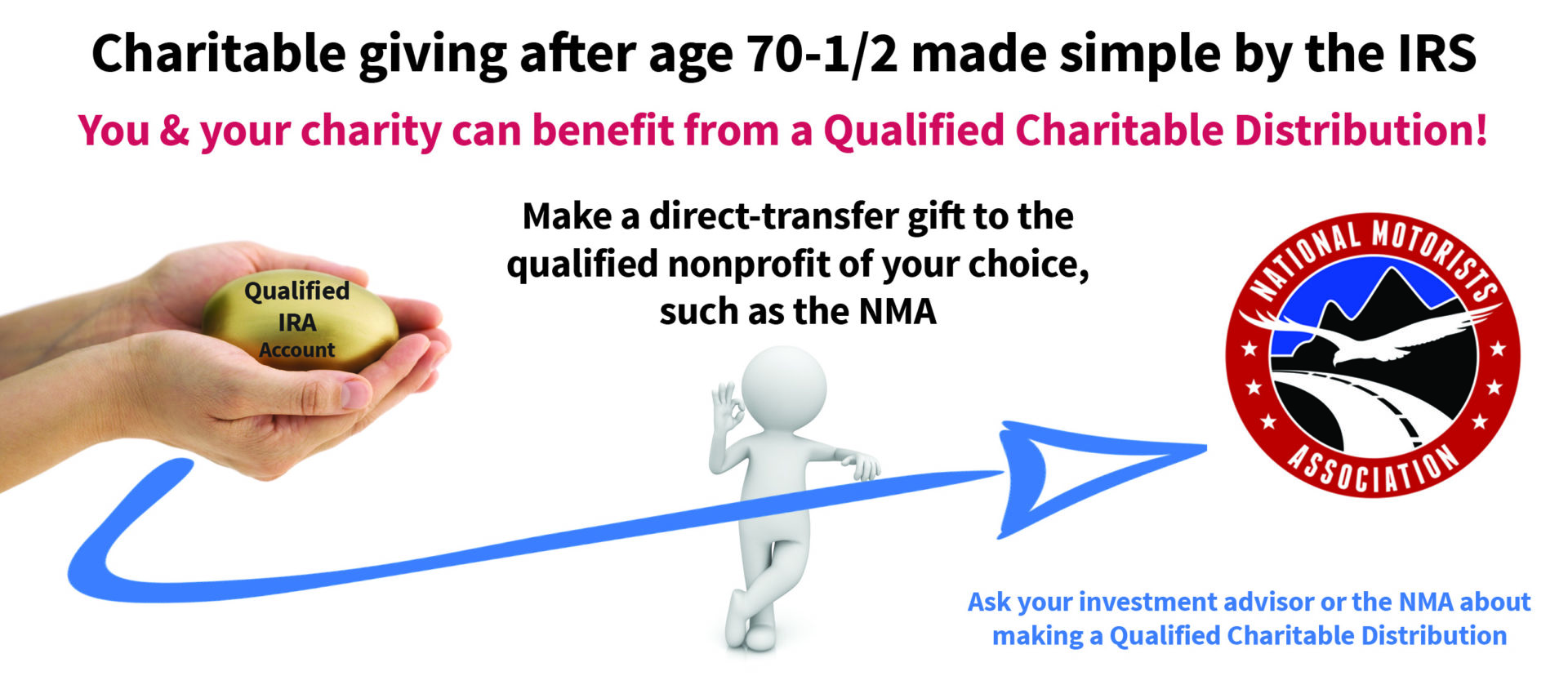

If you are are 70-1/2 or older, a Qualified Charitable Distribution from your traditional IRA, SEP or SIMPLE individual retirement account (IRA) can provide a benefit to you and for the qualified charity or charities of your choice.

A QCD is an otherwise taxable distribution from your qualified IRA — 401(k) plans are not eligible — that is transferred directly from the IRA account to a qualified nonprofit, such as the 501(c)(3) National Motorists Association. You must be at least 70-1/2 years of age to take advantage of the QCD provision. The total you donate in this manner must not exceed $100,000 in any given year.

Let’s say you are in the 25% overall tax bracket, and hypothetically you are considering donating $10,000 to one or more nonprofits from your qualified IRA account. (These examples do not apply to Roth IRAs, from which QCDs can be made under certain circumstances, because distributions from those accounts are not taxable.)

CASE 1: Withdraw $10,000 from Your IRA and Make No Donation

Your taxable income increases by $10,000, and your tax liability increases by $2,500. There is no charitable benefit.

CASE 2: Take Possession of the $10,000 from Your IRA and Donate It to a Nonprofit

Withdraw the $10,000 you wish to donate and put it into your bank account. Write a check to a nonprofit for $10,000. Your taxable income increases by $10,000, and unless you itemize your deductions, your charitable donation provides you with no tax benefit.

CASE 3: Donate the $10,000 in a Direct Transfer from Your IRA to a Nonprofit

Donate $10,000 to a nonprofit, like the NMA, by transferring the funds directly from your retirement account without taking possession. The charitable donation reduces the amount of the taxable IRA distribution to you by $10,000, whether you itemize your deductions or not.

As you can see, you benefit by transferring your charitable donation directly from your qualified retirement account to the qualified nonprofit of your choice.

PLEASE NOTE:

There are legal requirements you must meet so we recommend discussing these matters with your personal tax advisor before taking any action.

Because of the COVID crisis, the IRS has eliminated the required minimum distribution (RMD) for 2020. When the IRS lifts that exemption, the ages at which RMDs must be taken will be 72 and above. But individuals, as noted above, still can take advantage of the qualified charitable distribution starting at age 70-1/2.

If you choose to make a qualified charitable distribution to the NMA, contact the holder of your IRA account for the necessary QCD form. With mail delays commonplace now, it is best to request an electronic copy of the form which you can then return in a timely fashion. It generally takes a couple of weeks to process QCD requests, so be sure to turn your form in well before the end of the year to take credit for a 2020 distribution.

You will need the NMA’s bank account information, i.e., routing and account numbers if you choose an electronic transfer of funds directly to the account rather than have your IRA broker mail a check to the NMA. We’ll get those to you immediately upon request. Additionally, your IRA account broker will need the following information from the National Motorists Association:

NMA Federal tax ID number

39-1951971

NMA Corporate Address

1001 Arboretum Dr, Suite 120

Waunakee, WI 53597-2670

Thank you for considering the NMA when planning your charitable donations.